Collaboration between Neptune Mutual and SushiSwap

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Youtube Video

Playing the video that you've selected below in an iframe

Why capital requirement matters: What happens when more capital is required than there is capital?

Let’s start at the end with why capital requirement matters: What happens when more capital is required than there is capital?

Avid Neptune Mutual blog readers will have read one of our recent articles, Don’t Be a Salmon in a Bear Market, and recall a line that reminds us that “the stability of any stablecoin largely depends on what the collateral backing it up may be.” It goes on to describe how some stablecoins have zero collateral in terms of real-world assets, and others, such as BUSD, are 100% collateralised with real-world assets. This matters when, for one reason or another, a larger than expected call is made by depositors to withdraw their funds. As holders of the 2022 UST crash found out a couple of weeks ago, collateral, or capital requirement, really does matter — a lot.

Capital requirement matters greatly for entities that are either receiving deposits and making loans, or entities that are receiving underwriting capital and selling insurance, cover policies, or products that hedge other types of risk.

As any parent will know, it is difficult to share your hard-learnt life lessons with your children in a way that will help them avoid making the same mistakes. Some may recall the financial instrument that caused the 2008 financial meltdown and the bankruptcy of Lehman Brothers: CDOs or collateralized debt obligations that were used to refinance mortgage-backed securities; or even more toxic, synthetic CDOs. The keyword here being collateralized.

A more recent event, in 2021, albeit very different in nature, was the short squeeze inflicted upon a large American hedge fund, Melvin Capital, by an option trader community in the r/wallstreetbets subreddit. In an unexpected scenario, Melvin Capital ran into difficulties regarding insufficient capital to meet its much-maligned short trading bet against the infamous video game retailer, GameStop.

Without a doubt, capital requirement does indeed matter.

So, let’s dive into the two different approaches to balancing the need for sufficient capital versus the need to use capital efficiently so that it may be put to work and generate revenue:

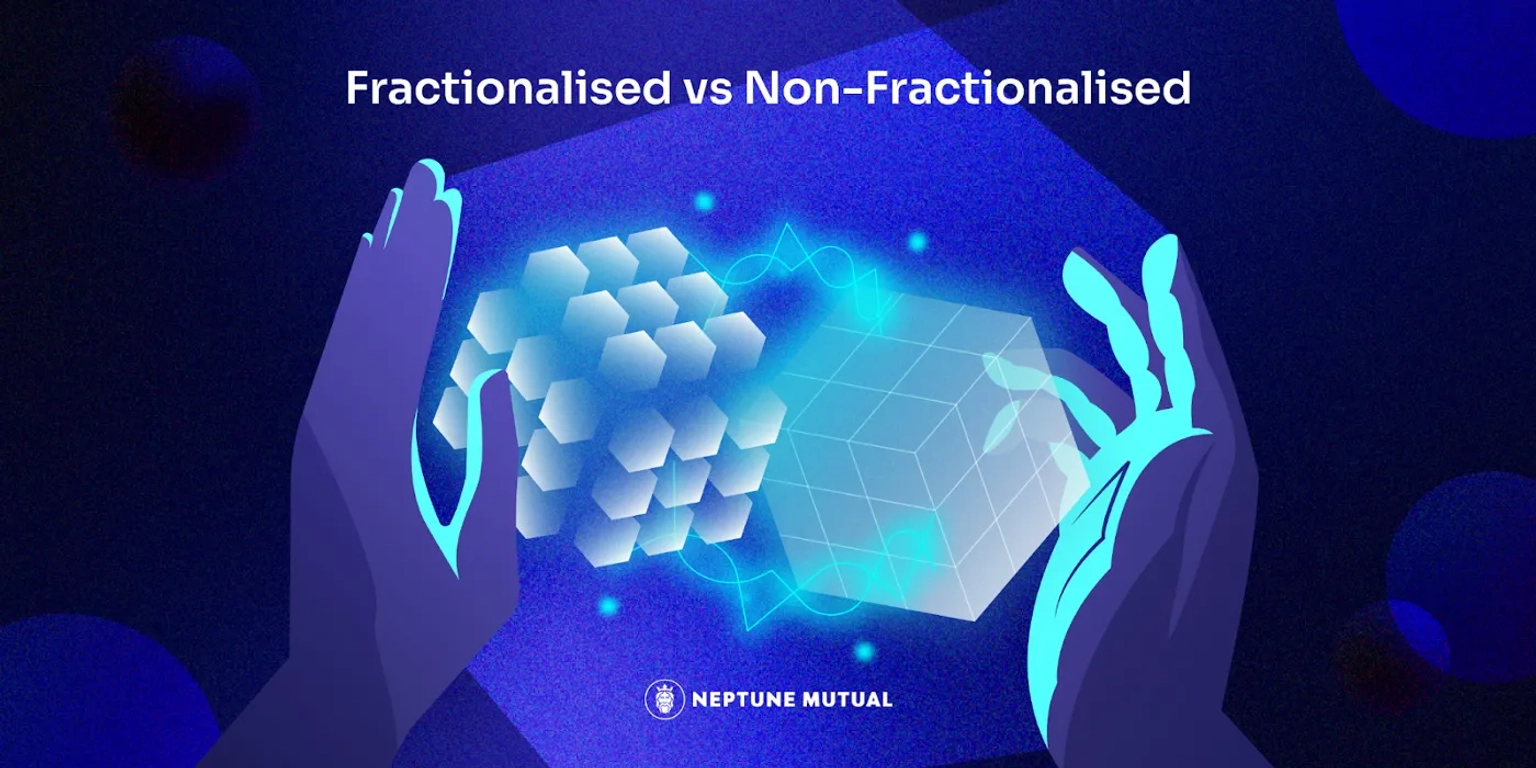

Fractionalised reserve systems are financial systems that maintain only a portion of their customers’ funds in their reserves.

The concept was first introduced in the banking industry. As the name suggests, fractional reserve systems only have a fraction of their bank deposits available for withdrawal by customers because the remainder of the deposits is used to lend out to other customers. Put another way, a 100% reserve bank retains all deposits from its customers (as the name suggests) and so is able to guarantee that in the event that every customer wants to withdraw their respective deposits at the same time, they can do so. This approach means that a 100% reserve bank does not have sufficient capital from depositor funds alone to be able to make any loans. In turn, this means that whilst being very safe, it will not be able to generate revenue from loans to pay depositors an interest rate on their deposits.

In a fractionalised reserve system where, for example, a bank has a reserve requirement ratio of 10% (i.e. is only required to keep 10% of customer deposits in reserve). If someone deposits $100 to this bank, the bank can lend out $90. If the borrower of that $90 deposits that back to the bank again, the bank can now lend out another 90% or $81. Whilst this scenario is unlikely in the traditional banking system because lending rates are higher than deposit rates, this mechanism is definitely something that you’ll find in the DeFi sector. Looping is a mechanism that quite a number of yield aggregators use to achieve high levels of leverage to generate high yields from a variety of borrowing and lending protocols and stablecoin currencies.

The Minimum Capital Ratio or MCR dictates the very lowest level of reserves required by financial regulators.

The insurance industry also adopted fractionalised reserve systems as it enables more efficient use of capital.

As with banking and traditional finance, the insurance industry is regulated and requirements vary depending on geography, market sector, and the corresponding regulatory requirements. In Europe, EU insurance companies need to comply with the Solvency II Directive which provides codes and regulations in respect of capital requirements including MCR and SCR which we’ll talk more about later on.

Based on current regulatory standards, an insurance company needs to calculate its capital on hand against its total underwriting liabilities. They need to meet a minimum level of required capital on their balance sheet based on the forecasted payout of liabilities that may arise over the next foreseeable future, say one year. This means regulation could require an insurer with an underwriting liability of $100 million to hold 10M$ on its balance sheet.

Like banks, different insurance companies use different models.

The leverage effect of a fractionalised reserve approach is attractive because it makes use of the capital in a more efficient way to generate returns for underwriters than a non-fractionalised system. In order to mitigate the risk of using 1 dollar to underwrite several dollars of risk, it is important for insurance companies to ensure that those risks are diverse in nature in order to reduce the likelihood of them arising at the same time.

The extent to which entities leverage their fractionalised reserve system in combination with their ability to manage and diversify the risks that are underwritten combine to form the entity’s exposure to insolvency.

Pros of Fractionalised Reserve Systems

Cons of Fractionalised Reserve Systems

A non-fractionalised reserve system can be used when the need for capital security and less, or no financial leverage outweighs the benefits of more capital efficiency.

For insurers, this means that underwriting capital is always equal to or greater than the total amount of underwriting liability. This ensures that there is always sufficient underwriting capital to pay all of the risks underwritten for policyholders, even if they all claim at the same time.

Minimum capital ratio, or MCR, is one of a number of metrics used to help answer the question, how do you measure capital requirement?

To start with, it’s important to understand the concept of solvency. According to Investopedia, solvency is a measure of capacity used in fractionalised reserve systems to find out whether a business can meet its debts, liabilities, and financial obligations in the long run. It is a reflection of business financial health.

Through the use of requirement ratios, investors can assess the solvency of a business and its capability to sustain operations. Requirement ratios help businesses to maintain a financial position that is safe and solvent. One of these requirement ratios includes MCR.

MCR is a term used in fractionalised reserve systems to determine the minimum required value of assets that a business must hold. MCR is regarded as a business’s capital requirement ‘hard’ floor in regulation. Once a business falls below the required Solvency Capital Requirement, or SCR (the other ‘soft’ floor requirement ratio), regulation intervenes to ensure that businesses don’t go below the MCR; failure to comply may incur regulatory actions to stop the entity from getting further out of line with its compliance requirements.

For traditional insurance models that use fractionalised reserve systems, MCR is a standard metric. In DeFi, several cover protocols adopt MCR as a metric.

Considering that the global DeFi ecosystem is relatively young there is not yet sufficient historical data to simulate the probability of loss reliably, and therefore it is not possible to calculate (with sufficient statistical significance) a reliable price point for this risk.

When considering what type of capital requirement model Neptune Mutual has adopted, it is important to note that Neptune Mutual uses a parametric cover policy approach which is quite different from a basket of risks underwritten by a common set of underwriters using a discretionary model. As the parametric approach to financial protection has a different risk profile to traditional insurance pools, MCR is not well suited for parametric protocols like Neptune Mutual.

So, Neptune Mutual Protocol V1 follows a full reserve system (or a non-fractionalised one) that maintains 100% of the capital in stablecoins against the total amount covered for cover policyholders by any specific cover pools in the platform.

If you purchase a cover from the Neptune Mutual platform and become a policyholder, you’re guaranteed that any and all claims you make get a payout instantly once the incidents covered by your cover pool are resolved.

It is integral to the purpose and mission of Neptune Mutual that our cover protocol puts you, our users, and cover purchasers’ interests first above all else and ensures that we can make a payout immediately when needed. Discover how our platform makes this possible through protocol parametric protection. You can also learn how to purchase a cover on Neptune Mutual.

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Learn about the effective strategies to protect your intellectual properties in Web3.

Understand the aligning of Neptune Mutual with Arbitrum for enhancing cover protection.