Collaboration between Neptune Mutual and SushiSwap

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Youtube Video

Playing the video that you've selected below in an iframe

Understanding the basics of parametric cover protection and it's major benefits.

The crypto market is often volatile. This means delays that get compensated for losses can be highly problematic. A challenge traditional insurance models are struggling to surpass.

Protocol parametric protection offers a simpler alternative with defined terms and wider coverage. More importantly, it is versatile and flexible enough to accommodate changes in an evolving digital assets market.

Blockchain-based digital assets are transforming how financial markets operate and how users all over the globe interact with financial systems. And what a wild ride it has been. From zero market value less than 15 years ago to a total value estimated at over $3 trillion in 2022.

However, this growth has been accompanied by a corresponding increase in risks. Cyberattacks and data breaches worth billions of dollars in the digital assets space strike fear in the hearts of market participants and stakeholders.

Decentralised protocol cover might provide the necessary safety net that investors and stakeholders need to protect their digital assets and transact with more confidence.

But first, what are these digital assets worth protecting?

The digital assets market and underlying blockchain technologies are evolving rapidly; this makes it difficult to establish a precise definition and categorisation of digital assets. Given the rate at which the market changes it doesn’t take long before definitions become out-of-date.

As it stands, the simplest way to describe digital assets is that they represent value in digital form. From a regulatory standpoint, the Swiss Financial Market Supervisory Authority (FINMA)focuses on the economic function and purpose when defining digital assets. It also classifies tokens in terms of three primary categories:

All categories of digital assets are subject to risk. In addition to the risk of targeted hacks and data breaches, the market is inherently volatile, which presents its own set of risks. There are also risks in terms of custody, technology flaws, asset valuation, and regulatory change, amongst others.

However, based on how much has been lost so far, DeFi digital assets have proven to be the most targeted over recent years:

Despite their swift growth and mass adoption, DeFi projects are among the most hacked blockchain protocols in recent times. In 2021 alone, the total value locked (TVL) in DeFi projects rose from around $18.2 billion to well over $243 billion. But in the same period, over $1.3 billion was lost to criminals, according to CoinDesk.

In a related analysis, DeFi project hacks are reported to account for around 76% of major hacks in 2021.

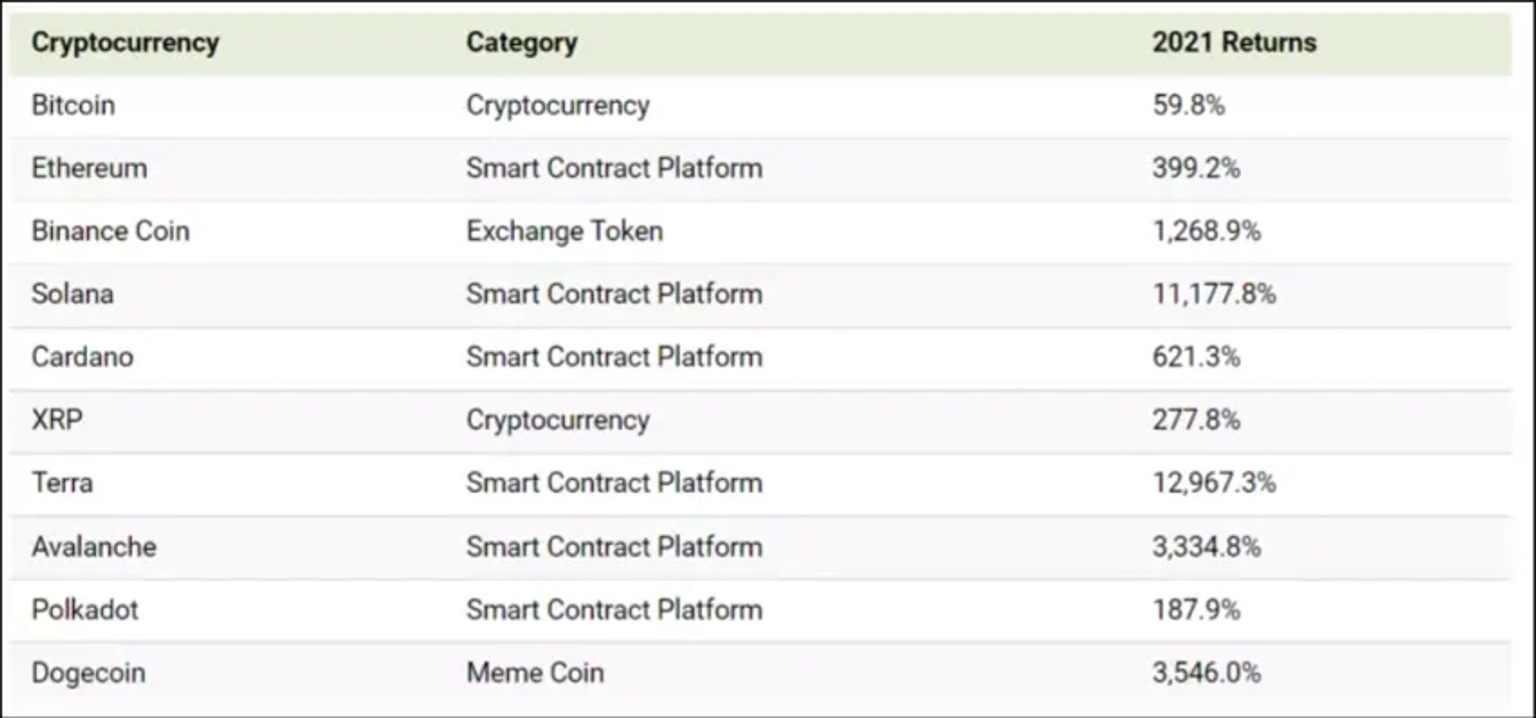

Crypto markets have been flourishing since Bitcoin made its debut in 2009. Following Bitcoin’s halving in 2020 the cryptocurrency’s total market capitalisation grew by over 59% over the course of 2021, and other cryptocurrencies recorded even more impressive gains.

However, where there’s money, you can expect that there will be people trying to steal it. In a recent report by Business Insider, hackers made away with over $4 billion in cryptocurrencies in 2021, which is almost three times what was lost the year before.

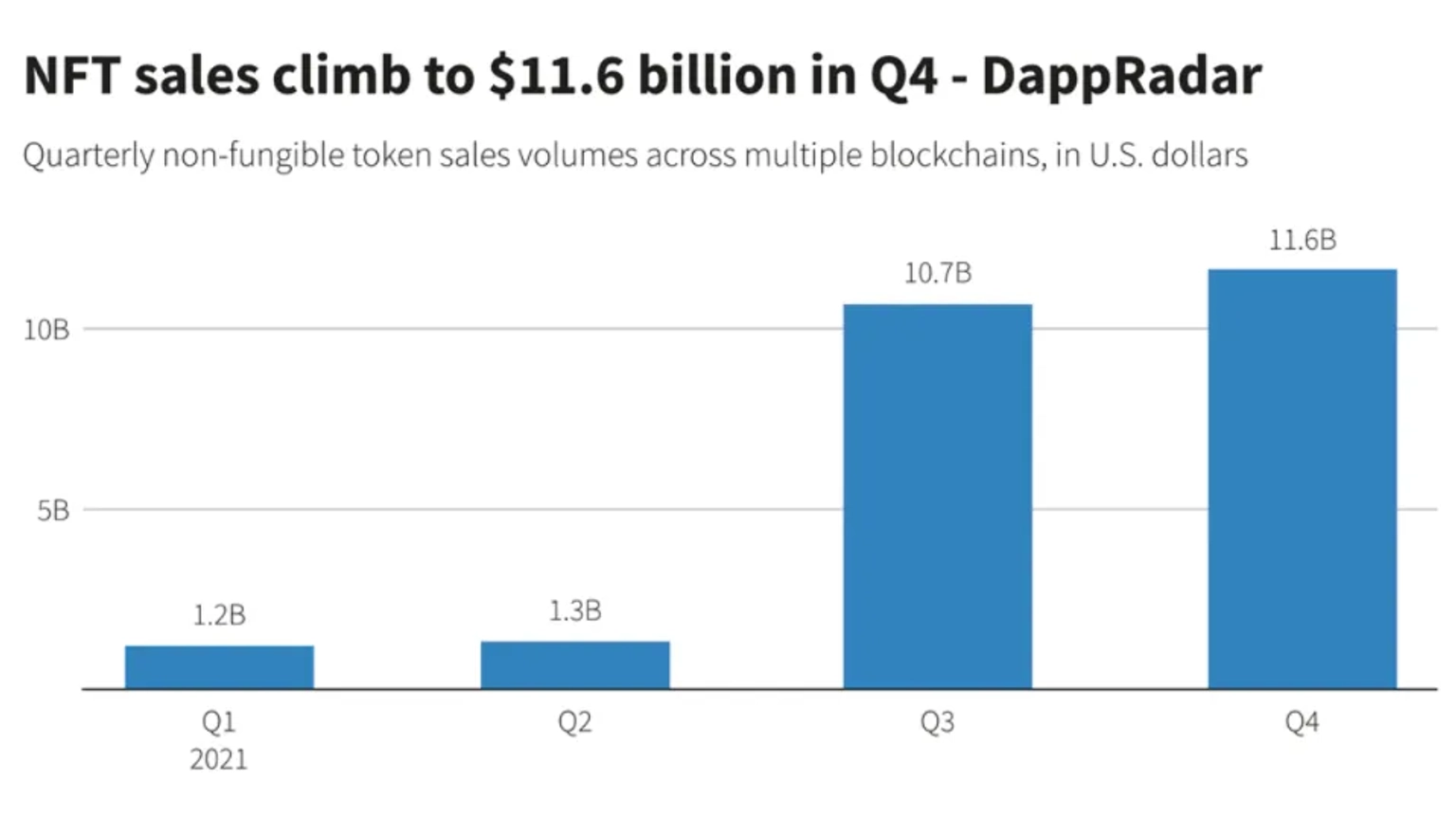

In 2021, sales of NFT tokens reached an amazing $25 billion, with over $11 billion being generated in Q4 alone.

Even though NFTs and Metaverse projects are relatively new, hackers have wasted no time in exploiting vulnerabilities and carting away millions of dollars. In February 2022, the world’s largest NFT marketplace, OpenSea was hit by a phishing attack that saw users lose NFTs worth over $1.7 million. One month later, an attack on the Ronin bridge system for the popular NFT-based game, Axie Infinity, lost over $600 million following a network breach.

The reality for digital asset owners is that nothing is 100% secure. Even if they adhere to all the security best practices, other risk elements, such as code exploits, flash loan attacks, human error, and rug pulls, remain ever-present.

Cover protection can become a crucial factor in mitigating these risks and facilitating an environment where market participants can initiate transactions more confidently. But while traditional insurance has been pivotal in improving risk management and operational efficiencies in finance, progress has been slow when it comes to protection for blockchain-based assets.

In part, this is due to the different nature of digital assets and the ecosystem within which they fit. Peer-to-peer digital asset transactions in reality often take place wallet-to-wallet where there is no information available about either party, and this obviously doesn’t work well in a traditional insurance model context where you need to prove your identity, your ownership of an asset, and prove that the loss of you have suffered conforms with the terms of your policy.

This leads to another issue relating to the blockchain ecosystem and digital assets which is that frequently the digital assets and the risks they are exposed to are highly technical, and equally importantly the exclusions that relate to policies are also highly technical. It can often be far from clear to policyholders what risks their policy protects them against, and what it does not. This can lead to situations where users pay for policies and expect to receive a payout as a result of a hack or exploit, only to find that the specific technical nature of the exploit was excluded from their policy.

This lack of clarity about what policies cover has accelerated the need for a new approach, namely, parametric cover.

From the name alone, it’s easy to get a general idea of what parametric cover is all about. It’s a type of policy that provides a financial payout conditional on a set of parameters that define the risk events that the policy protects against. When these predefined parameters are met, the policyholder automatically receives a predefined payout.

Because payouts are tied to predefined parameters being met, the insurance policy is disconnected from an underlying asset, as well as any damage or losses sustained on that asset. In other words, instead of trying to quantify losses to determine whether a payout should be released and how much, the insurer only needs confirmation that the event leading to the loss indeed occurred, in order to make the agreed-upon monetary payment.

Parametric coverage offers many benefits, including:

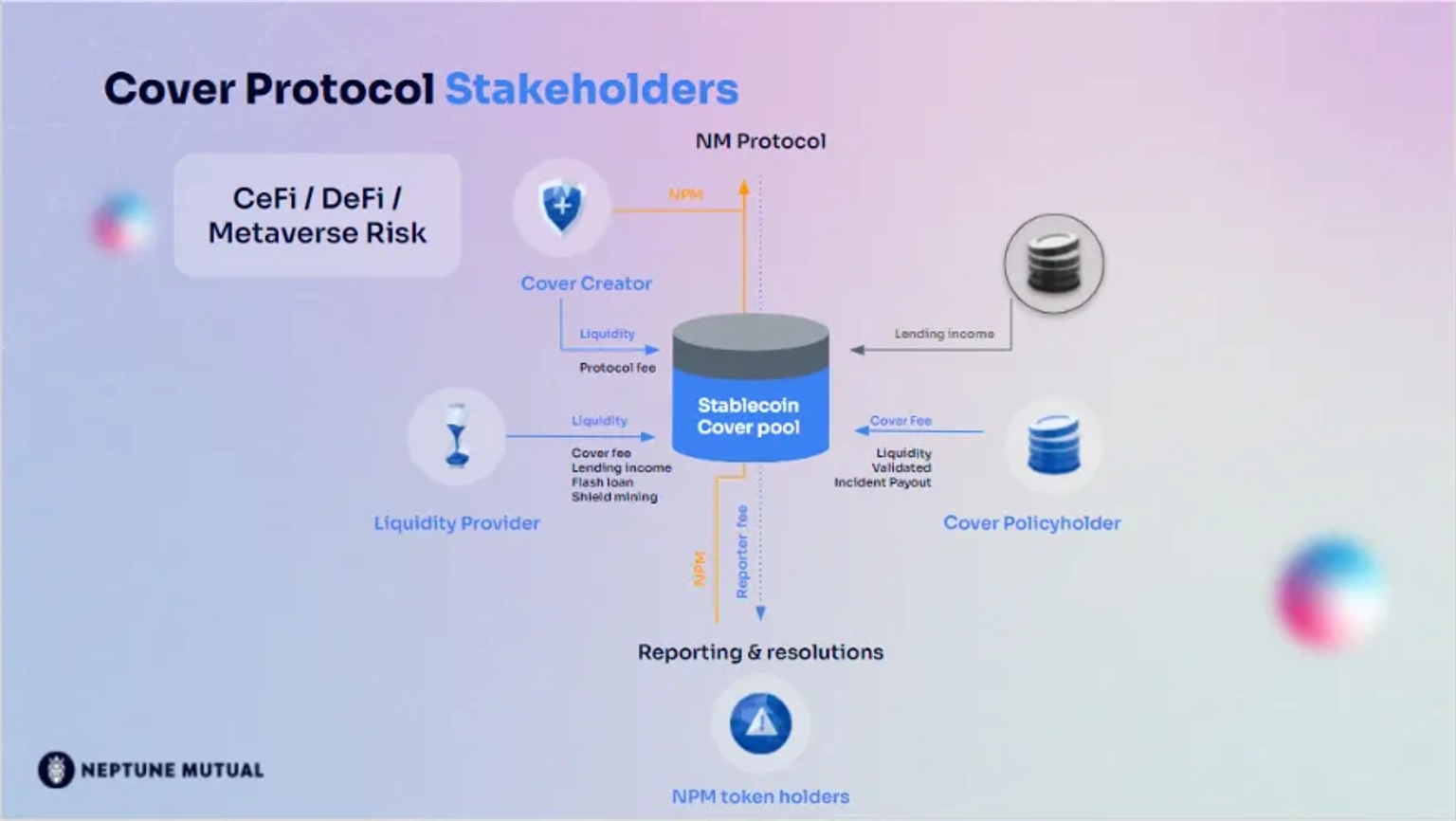

The Neptune Mutual ecosystem is built on four founding principles — security, scalability, risk minimisation, and user experience. Together, they create a conducive environment for stakeholders to facilitate the exchange of value within the system.

There are four primary stakeholders:

Under the Neptune Mutual ecosystem, cover creators can generate parametric-based cover protocols with guaranteed stable coin liquidity to cover losses resulting from specific hacks or smart contract vulnerabilities.

By providing liquidity into cover pools these stakeholders earn a variety of income and rewards. Income from the protocol includes cover policyholder fees, flash loan interests, and lending incomes arising from loans of “excess” capital within the pool. Other rewards for liquidity providers can come in the form of staking rewards, native project tokens, and discounted NPM tokens.

These stakeholders are integral to incident governance and reporting. Using a fair, transparent, and efficient system, NPM token holders vote to confirm whether a triggering incident occurred or not. The resolution is made within 7 days of the incident.

Anyone can become a policyholder by connecting their wallet to the platform, navigating to a cover pool, selecting the cover amount and duration, and confirming the transaction.

If an incident occurs that appears to fall within the scope of the cover parameters, it will be reported and be subject to the community incident validation process that determines whether or not a cover pool should payout or not.

If a cover incident is validated by the community then a payout to ALL policyholders of that cover pool is guaranteed.

Once the incident report process is initiated, withdrawal of liquidity from the cover pool is automatically suspended. The rules of the protocol are such that there is always more liquidity available in the cover pool than the total liability underwritten by cover policyholders’ payout; this ensures that there will always be sufficient funds in the pool to cover all valid claims.

Cover creators can set up new dedicated cover pools by staking NPM tokens, the fixed and deflationary native token of the Neptune Mutual ecosystem.

The minimum stake required to initiate the cover creation process is 4,000 NPM tokens. The more NPM tokens staked by the cover creator, the better the cover pool’s ranking and visibility on the Neptune Mutual product list.

The cover creation process itself is straightforward and can be broken down into three simple steps:

What are the parameters of the risks that the cover will protect against? What are the exclusions to those parameters? Generally speaking, the fewer and more specific the parameters, the better. The parameters also need to be binary, that is to say, either true or false. Exclusions should be kept to a minimum and typically include: deliberate and malicious actions by the project team; or, acts of gross negligence on the part of the project team.

Let’s say a cover creator wants to create a parametric cover pool for their DeFi lending platform. They might include a parameter that states that if a smart contract code is hacked and the amount lost is over $10 million. If any of these parameters are fulfilled, the incident resolution and payout process are automatically triggered.

Price the Cover

This involves setting up a pricing spreadsheet containing a number of variables that influence policy pricing offered by the cover pool. Examples of these factors include floor and ceiling price, cover commitment, and reassurance pool support, just to name a few.

Many cover creators that are confident in the security of their projects will want to provide confidence to liquidity providers through a reassurance mechanism. This is one in which a reassurance pool that is financed by the cover creator is used to recapitalise the liquidity of the cover pool (up to a certain percentage) in the event that a validated incident arises causing liquidity to be drained from the pool. It is provided by cover creators to provide a layer of protection to the capital provided by liquidity providers.

The cover pool will require enough liquidity to get it started. There are different ways to go about this. Usually, cover creators will invest their own capital to kickstart the process of attracting liquidity. They will also attract liquidity providers through the use of the numerous features available on the platform, including staking and proof-of-deposit (POD) staking programs, and so on.

Neptune Mutual and cover creators will work closely together to communicate the value of parametric protection to their respective communities. Putting in place a solution that can rapidly provide a payout in the event of a hack or exploit demonstrates a mature and considered approach to risk management as well as a sensible and respectful way of looking after the interests of a community.

Neptune Mutual recently launched its protocol testnet on the Polygon network. Users can sign up to test various functions of the ecosystem, including validating incident reports and claiming cover policy payouts.

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Learn about the effective strategies to protect your intellectual properties in Web3.

Understand the aligning of Neptune Mutual with Arbitrum for enhancing cover protection.