Collaboration between Neptune Mutual and SushiSwap

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Youtube Video

Playing the video that you've selected below in an iframe

Learn about why the insurance cooperation is required now than ever in a blockchain industry.

Onchain insurance is a much-needed solution for risk management in the blockchain space. However, amid evolving risks and user expectations, the need for cooperation over competition among cover protocol providers has become more evident.

Can this change of approach promote more effective onchain cover solutions and improve confidence among stakeholders? We certainly think so.

Cooperation has always been foundational to success within any ecosystem. There’s no reason why it shouldn't have a role to play in establishing the value that onchain insurance brings to the blockchain space.

Admittedly, cooperation and collaboration are not always common practices in the industry. But given that blockchain is still relatively new to the party, perhaps now’s the right time to re-examine what we know and see if doing things a little differently can get us more desirable results.

Due to its decentralized nature, blockchain technology presents a number of unique challenges for insurers, such as data privacy issues, underwriting risks, claims validation processes, and lack of a standard regulatory framework, among others.

And while protocol cover providers have found clever ways around these issues, adoption of these solutions is still very limited. One can’t help but wonder if collaboration between protocols might not help raise awareness and change behaviours towards more widespread adoption of digital asset protection. As we see so regularly in news headlines about huge losses, there is clearly a strong case for protecting digital assets.

With a projected growth rate of more than 72% over the next six years, the global blockchain market continues to thrive with more participants coming into the scene every day. But it is not just the sheer volume of investments by millions of investors around the world that make the space valuable.

The blockchain ecosystem is highly segmented – payments, smart contracts, digital identity, governance, digital voting, documentation, exchanges, and many others. Each segment brings a new wave of applications which offer the potential to completely transform how we do things. These applications are what drive value in the space.

Like its off-chain counterpart, onchain insurance seeks to provide cover against risks. These risks manifest themselves in different forms and can impact almost every facet of the blockchain space, including:

A Multibillion Dollar DeFi Market

Even with a prolonged bear market, the Decentralized Finance space has managed to maintain a market capitalization of over $39 billion.

Popular DeFi projects like Uniswap, Aave, PancakeSwap, and Chainlink have quickly attracted millions of users to their respective ecosystems. This means that there is a ready market for onchain insurance to safeguard against certain and uncertain risks.

A Rise in Code Exploits and Security Breaches

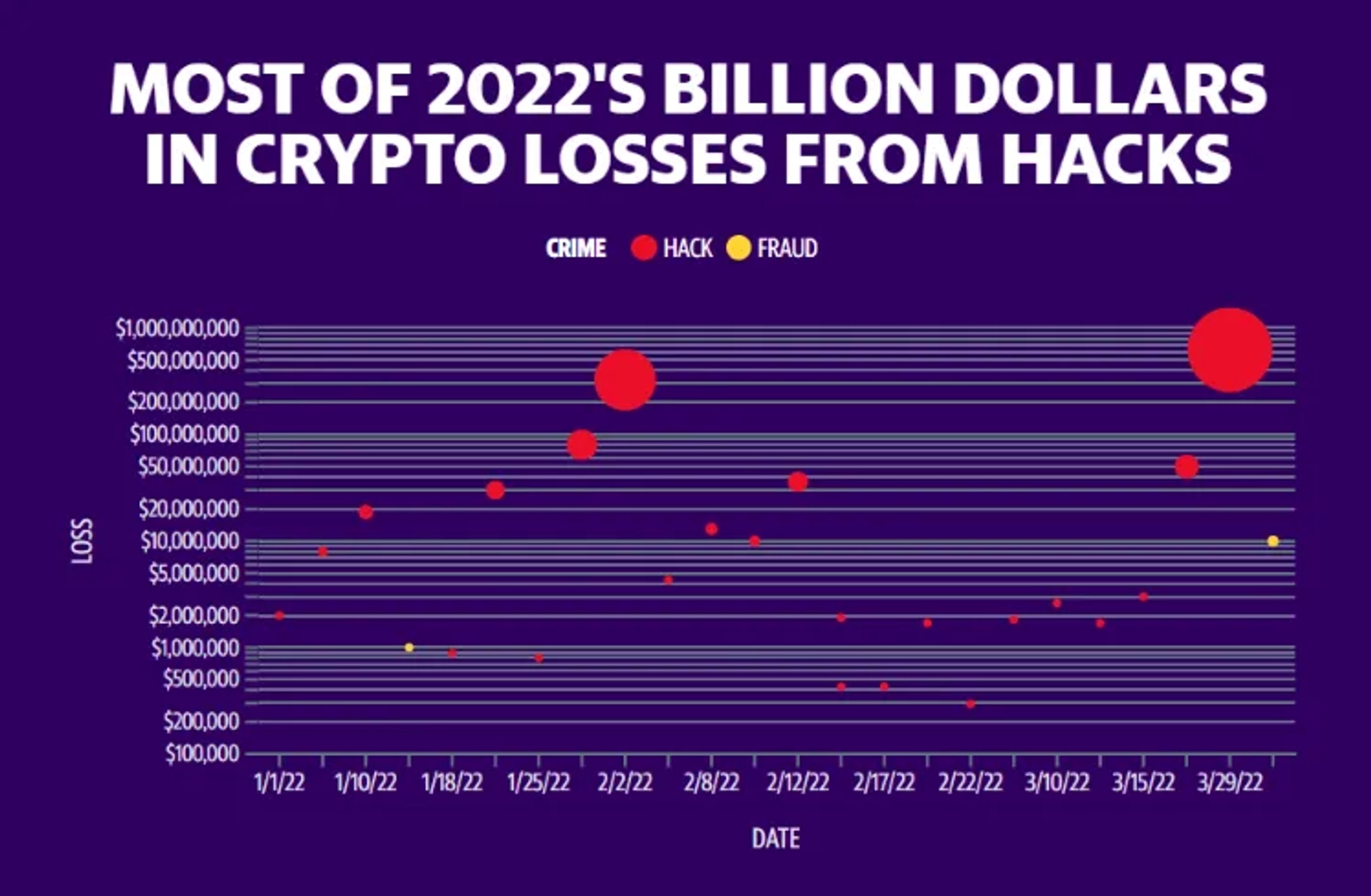

Cyber-attacks by hackers seeking to steal digital assets and commit other related unscrupulous activities continue to make headlines. In the first quarter of 2022 alone, over $1.2 billion has been lost to smart contract code vulnerabilities and security breaches.

The presence of onchain insurance to cover these risks can go a long way in allaying the apprehension of investors and in building trust between projects and their respective communities. It will also promote confidence in the viability of blockchain projects and their related transactions.

A Budding Metaverse Ecosystem

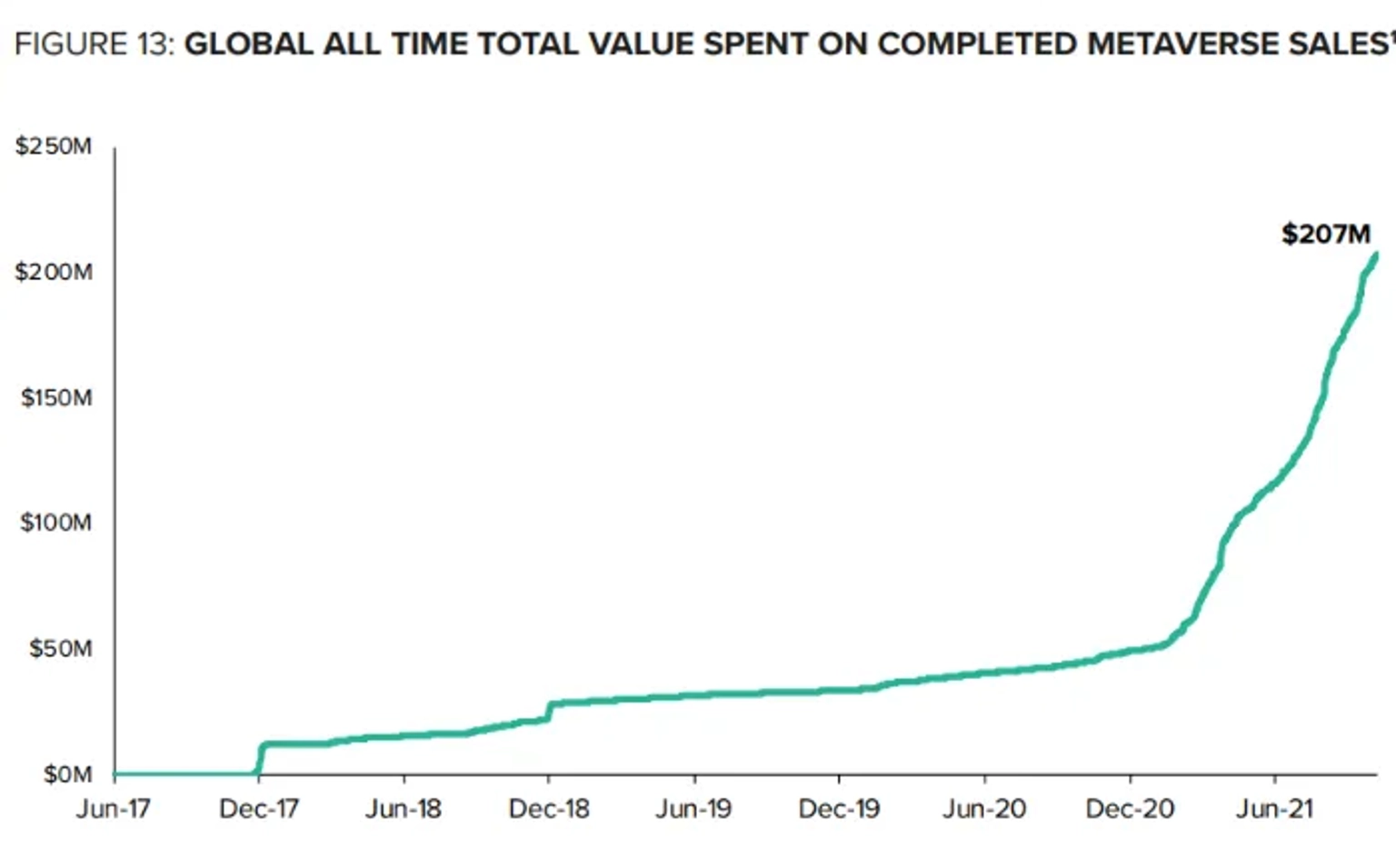

The metaverse is the future – at least that’s what tech entrepreneurs and investors believe. They’ve even gone as far as investing billions of dollars into the concept. Microsoft, Meta (formerly Facebook), Google, and Nvidia are just some of the leading tech giants to be actively involved in shaping the metaverse market, which is projected to be worth over $800 billion by 2024. Individual spending on metaverse projects and items is steadily rising too.

Non-Fungible tokens or NFTs, which are an integral part of metaverse interactions continue to attract heavy inflows as well, with some NFTs commanding tens of millions of dollars in the open market.

As more individuals scramble for these digital assets and collectables, onchain insurance will play a critical role in providing cover against uncertainties, as well as facilitating trustless transactions.

Onchain insurance is still nascent and the pioneers are working hard to forge a path through new terrains laden with challenges at every turn. There’s no better time for collaborative efforts than now. And while competition breeds creativity and innovation, the industry has far too many issues that if not addressed now can continue to plague onchain insurance for years to come.

Of course, the scope of the cooperation among cover protocols will be tailored for mutual benefit, but there’s no denying that there’s merit to the idea.

Here are some areas where insurers on the blockchain can bridge gaps and deliver more value across the entire ecosystem.

Because onchain insurance is built on emerging technology, it is subject to emerging risk. With so much money coming into the space, the probability of hacks is always there. In fact, one may argue that hacks are a necessary evil in blockchain because they expose flaws within a project's security system and lead to better code infrastructure development.

But with more efficient information sharing among cover protocols, it’s easier to prepare for these risks. As soon as a hack occurs, all other protocols know about it and add that to their checklists to make sure they don't fall victim.

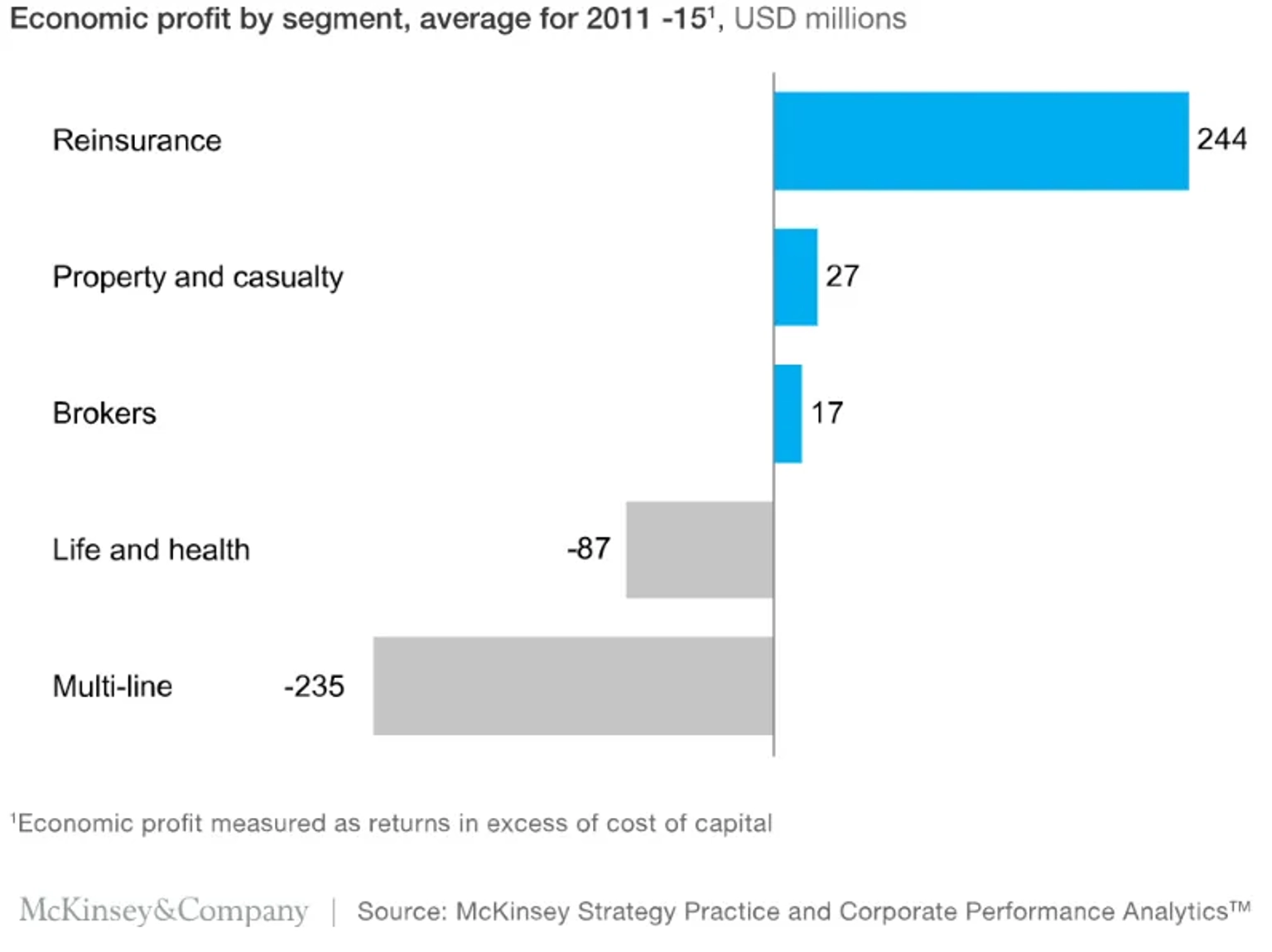

Insurance for insurance companies – that’s basically what reinsurance is all about. It’s a stop-loss insurance that lowers underwriting risk for insurers and helps them remain solvent by recovering a portion of amounts paid out on insurance claims.

Reinsurance is already common practice in real-world insurance, having been a critical part of the global industry for over 150 years. It has also outperformed other segments in the overall insurance space in recent times according to a 2017 report on Global Reinsurance by Mckinsey and Company.

You’ll agree that reinsurance is a necessary component in the blockchain space. It decreases risk to insurers by passing a portion of the underwriting burden on to others.

Reinsurance can also help stabilise losses, such as when a cover protocol has to pay for a large number of claims in a short period of time. This can leave them in a dire financial situation. Reassurance offers insurers the opportunity to benefit from a wide base of underwriting capital.

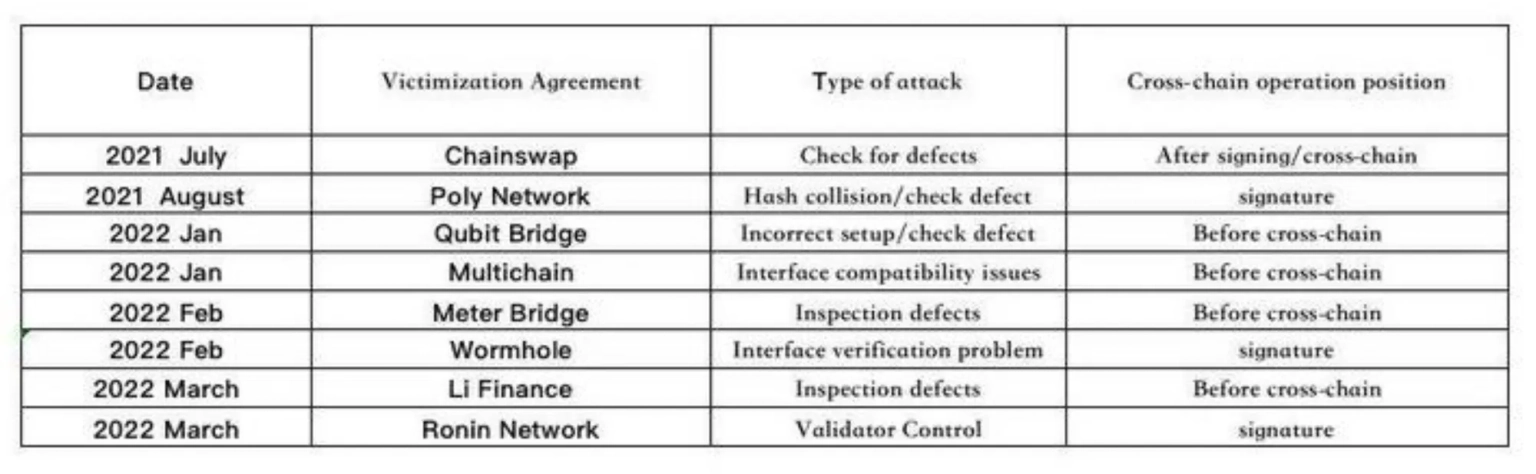

As the name suggests, a cross-chain bridge connects two blockchains so users can transfer digital assets and information from one chain to the other. Because cryptocurrencies and tokens are typically siloed to their native blockchains, bridges are a necessity in facilitating value exchange.

Because they handle such valuable transactions, it’s easy to see why the risks of security breaches are concentrated around cross-chain bridges. One of the biggest DeFi exploits in history was the result of a cross-bridge attack. The Wormhole bridge hack saw the loss of over ETH 120,000 ($321million at the time).

While it is not necessarily their responsibility to address this particular issue, onchain insurers are a key stakeholder in the security of cross-chain bridges. Lending their expertise to the matter can definitely help move the needle towards more viable and lasting solutions.

The blockchain space is characterised by a strong sense of community, and so having the brightest minds in the onchain insurance industry coming together to help make it a better protected place should be a positive outcome.

The success of insurance protocols is likely to be driven more by widespread adoption of digital asset cover. To make this happen, it’s important to take a step back and examine what factors influence adoption of new technologies: we examined this issue in our blog Crypto Crash Heightens Awareness of Risks & Hacks, But Is This Enough to Drive Mainstream Adoption of Digital Asset Protection?

According to a PwC report, the top driving factors of blockchain adoption are provenance, improved access to payments, and customer engagement.

To a certain extent, these elements are also crucial to adopting onchain insurance.

Provenance in the form of authenticated incident reports and claims validations; streamlined financial transactions through efficient underwriting and payouts; and customer engagement in the form of improved top-to-bottom user experience and careful consideration of UI (user interface) design.

These goals are generally more attainable when there is positive cooperation between existing insurance protocols.

As the onchain insurance grows in maturity, we can expect regulators to take a more active interest in the space. After all, the real-world insurance industry is one of the most regulated.

Most countries have wasted no time in drafting up regulatory guidelines for blockchain-related transactions.

At some point, it may be that regulations are expanded to include aspects of the operating activity of onchain insurance providers. And when that time comes, maintaining a collaborative approach between cover protocols can greatly help in moving these discussions in the right direction.

On April 21, 2022, Ethereum security firm Secureum TrustX, in conjunction with DevConnect Amsterdam, hosted a deep-dive discussion with some of the leading innovators in onchain insurance.

The session was chaired by Emiliano Bonassi of Rentable and included guest speakers – Dan Thomson of insurAce, Evert Kors of Sherlock, Hugh Karp of Nexus Mutual, Kiril Ivanov of Bright Union, and Robert Forster of Ease.

When asked about the possibility of cooperation among cover protocols with regard to reinsurance, Nexus Mutual’s CEO Hugh Karp had this to say,

"Yeah, I think it'll happen. I think that we will be seeing some reinsurance between different protocols… But I also think that there will be a point where we may actually go outside at some stage to get reinsurance from traditional markets. And, you know, philosophically that's not really where I want to be, but it might actually help us progress forward."

(Armor) Ease founder Robert Forster echoed the sentiment by stating

“I think we're gonna purchase some amount of reinsurance in the next week or so. With our system we need to be adequately diverse. We can't have faults having too much capacity in one way or another. So we need a little bit of reinsurance and I agree that eventually something off chain, something more traditional is going to be extremely helpful… Hopefully, there'll be more talks there regarding how we can work together.”

InsurAce’s director of marketing and business development, Dan Thomson also believes cooperation has an important role in moving onchain insurance forward, particularly with regard to regulatory frameworks

“Yeah, we agree working together is a feature we've actually been talking about this week though not necessarily this exact issue, but also about having to deal with regulators globally… A united front is a much better collaborative state to be rather than competitive.”

Lastly, Bright Union’s co-founder and technical lead Kiril Ivanov believes cooperation is a given in blockchain.

“It's a no brainer. With the composability of the blockchain, reinsurance is a given. If you want to launch your insurance product, you will definitely reuse some of the DeFi solutions out there…so collaboration is part of the blockchain nature.”

Complex evolving risks, more demanding customers, market disruptions, and other inherent issues require that onchain insurers move toward better collaboration. Working together will be crucial to meeting these challenges and developing specific value-add solutions within the ecosystem.

What the winning model of cooperation will look like remains to be seen, but it’s clear that it will require a combination of well-defined objectives and a strong commitment to achieve them.

Let us hear from you. What do you think about the need for cooperation over competition among onchain insurance cover protocols?

Explore Neptune Mutual's ongoing collaboration with SushiSwap offering several benefits.

Learn about the effective strategies to protect your intellectual properties in Web3.

Understand the aligning of Neptune Mutual with Arbitrum for enhancing cover protection.